A change is expected in Act 154

18 Sep 2019The first meeting between Governor Wanda Vázquez and US Secretary of Treasury, Steve Mnuchin (“Secretary”), triggered an anticipated request from the Secretary: the government of Puerto Rico has to identify an alternative to the 4% excise tax of Act 154-2010 (“Excise Tax”). With tax collections of around $1,800 million, the government faces the challenge it knew it would face sooner or later.

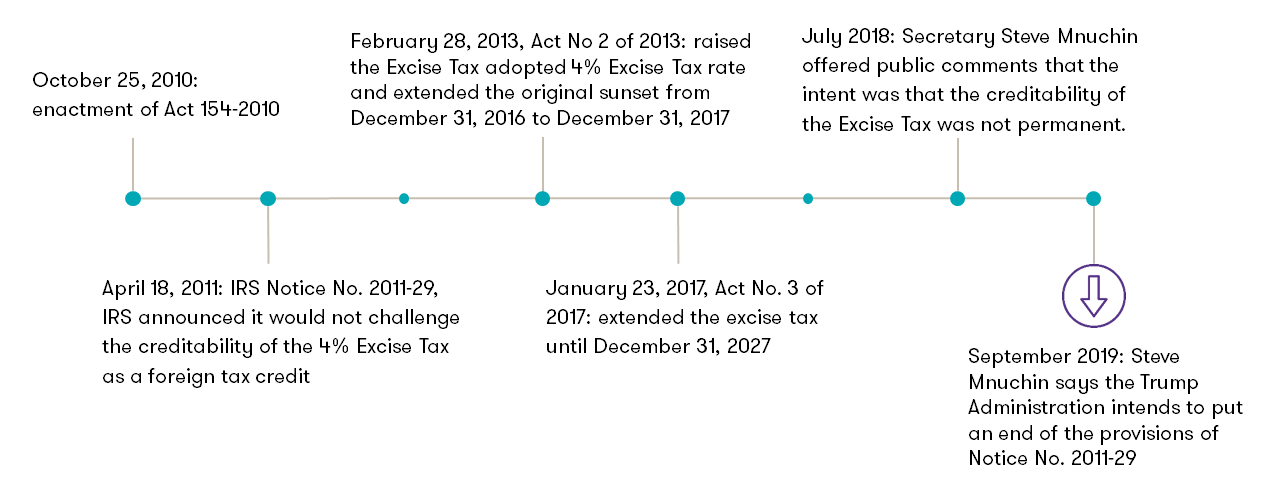

The timeline of Act 154-2010 is as follows:

See timeline CHART

Article 154-2010 timeline

Exise Taxes

The sudden enactment of the Excise Tax on October 2010, which was approved without public hearings, raised concerns regarding the creditability of the tax for US federal income tax purposes. However, other than a credibility and stability issue with foreign corporations doing business in Puerto Rico, the matter laid dormant because the practical effect of Notice No. 2011-29 was that the Excise Tax did not have a significant impact on the tax bills of affected taxpayers because they had a foreign tax credit in their US federal income tax return.

Since the core of the issue is in connection to the creditability of the Excise Tax for US federal income tax purposes, it is expected that the conversation will turn into what type of tax should be adopted that is creditable under the current rules of the US Internal Revenue Code (“US Tax Code”).

The US Tax Code

Currently, the US Tax Code has general provisions of foreign tax credits (“FTC”) and indirect foreign tax credits (“IFTC”). The FTC prevents double taxation of foreign income of US persons by reducing US tax on that income by the amount of income tax paid to foreign governments for example Puerto Rico. The analysis starts with whether the foreign tax is a creditable tax. Section 901 of the US Tax Code limits the credit to foreign taxes imposed on “income, war profits or excess profits.” AN FTC is also allowed for taxes imposed “in-lieu-of” a generally imposed income tax.

The IFTC applies specifically to controlled foreign corporations (“CFCs”). Section 960 of the US Tax Code generally provides that when undistributed earnings of a CFC are taxed to a domestic corporation as Subpart F income, the domestic corporation may be deemed to have paid a portion of the foreign income taxes paid or deemed paid by the CFC. Thus, a domestic corporation that is taxed on the earnings of a CFC may be able to claim an IFTC for foreign income taxes paid or deemed paid by the CFC to the foreign jurisdiction.

Section 951A

For taxable years of foreign corporations beginning after December 31, 2017, a US shareholder is required under §951A of the US Tax Code to include in gross income the “global intangible low-taxed income” (“GILTI”) of its CFC. In connection to IFTC, US corporate shareholders may claim an indirect foreign tax credit for 80% of the foreign tax paid by the shareholders' CFCs that is allocable to GILTI income.

The allocable amount of foreign taxes paid is calculated by multiplying an "inclusion percentage" by the foreign income taxes paid that are attributable to the GILTI inclusion. These credits have complex rules, which should be studied carefully as part of the analysis that will be done by the Government of Puerto Rico.

Presently, revenues derived from Act 154-2010 account for about 20% of the Puerto Rico General Fund. Therefore, all taxpayers should be wary of the issue at hand because there will be a need to identify funds for the Puerto Rico General Fund, and they may as well come from any one of us.

Please contact our Tax Department should you require additional information regarding this or any other tax issue. We will be glad to assist you.