For many years, there has been plenty of public discussion around incentives available to resident individual investors (“RII”) that relocate to Puerto Rico, and the last couple of months have not been the exception. This Alert will summarize important recent developments regarding RII incentives, with a focus on Senate Bill 490.

Senate Bills

- Senate Bill 40 - filed on January 4, 2021, authored by Senator María de Lourdes Santiago and Senator Jose Vargas Bidot – proposes the revocation of Act 20-2012 and Act 22-2012. Had three public hearings in the Senate during the month of July. The Department of Economic Development and Commerce appeared during the public hearings and submitted its position of not supporting the bill. Proposed effectiveness is upon the approval of the law.

- Senate Bill 284 - filed on April 5, 2021, authored by Senator Carmelo Ríos – seeks to amend Section 6020.10 of Act 60-2019 to eliminate the current rule that at least $5,000 of annual charitable contributions be destined to certain non-profits related to childhood poverty and included in a list of the Legislative Assembly. Rather, by eliminating such a condition, grantees would be able to donate $10,000 to the non-profit of choice. Had three public hearings in the Senate during the month of July. Proposed effectiveness is upon the approval of the law.

- Senate Bill 490 (“Bill”) - filed on July 13, 2021, authored by Senator Tomás Rivera-Schatz – proposes comprehensive reform to tax incentives available to RII. This alert will provide an overview of its most important provisions.

Senate Bill 490

Effectiveness

The effectiveness of the proposed law is upon the enactment of the law. The Bill indicates that it will apply to applications that have not been approved on the date of enactment of the law.

Proposed regime

The Bill restructures incentives available to new individuals with grants of tax exemption for RII (“Grant”). The tax rates offered will depend on whether the individual made capital investments that result in job creation in Puerto Rico, as discussed below. The statement of motives of the Bill recognizes the economic impact of incentives granted to RII. However, the Bill indicates, it is necessary to amend said provisions so that there is a better balance between attracting individuals to Puerto Rico, job creation, investment of capital in the island, and government revenues that can be reinvested in the Island for the benefit of all Puerto Ricans. The statement of motives also states that the Legislative Assembly respects obligations of the government of Puerto Rico in connection to existing grants but aims to create a more balanced scenario for new grantees by increasing tax rates while keeping them well below the national average.

Eligibility

Currently, individuals that were not residents of Puerto Rico from January 17, 2006 to January 17, 2012 are eligible to apply for a Grant. The Bill modifies this rule and establishes that individuals that were not residents of Puerto Rico during the five calendar years prior to his or her application for individual investors will be eligible for incentives.

Eligible Investment

The Bill proposes enhanced incentives if the RII makes an Eligible Investment. Eligible Investment is defined as follows:

- investment of capital - $5 million investment made on or after the date of filing the RII Grant application. The investment shall generally be completed within the 3-year period from the effectiveness of the Grant in exchange for equity in an Eligible Investment Entity. The latter term is defined as a domestic for-profit legal entity dedicated to the following activities:

- export services, pursuant To Chapter 3 of Act 60-2019

- Finance, investment and insurance, pursuant To Chapter 4 of Act 60-2019

- visitor’s economy, pursuant to Chapter 5 of Act 60-2019

- manufacturing, pursuant to Chapter 6 of Act 60-2019

- infrastructure and energy, pursuant to Chapter 7 of Act 60-2019

- Agroindustries, pursuant to Chapter 8 of Act 60-2019

- creative industries, pursuant to Chapter 9 of Act 60-2019

- other industries, pursuant to Chapter 11 of Act 60-2019

- job creation - the Eligible Investment Entity will be subject to compliance to the job creation provision, which requires the creation of at least 10 direct employees within a 3-year period from completed the Eligible Investment.

The Bill proposes rules that apply if an Eligible Investment Entity ceases operations. The grantee is required to complete an Additional Eligible Investment into an Eligible Investment Entity within a 12-month period and will be subject to the job creation rule applicable to the initial Eligible Investment.

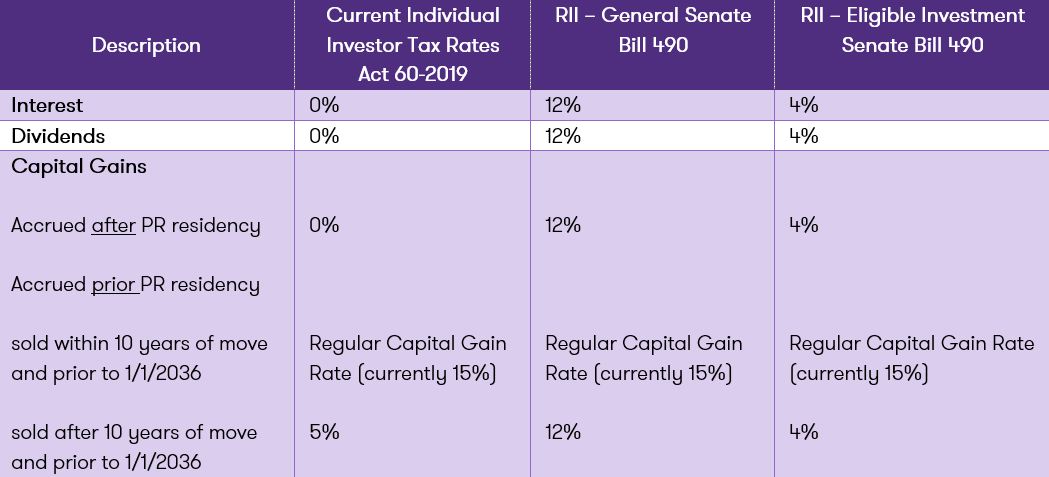

Incentives for RII

![imagep4ual.png]()

Other provisions

- penalties

- penalties of $10,000 for failure to comply with the requirements of the Grant (i.e. capital investment, job creation) will be imposed and should be payable within a 60-day period.

- financial commitment

- all grantees shall open a bank account in Puerto Rico that should be kept during the effectiveness of the Grant.

- annual report

- the November 15 date to submit an Annual Report is eliminated from the legal provisions related to annual reports and instead, the proposed language delegates the power to request information to the Secretary of Treasury.

- annual donation

- establishes that the $10,000 annual donation to a non-profit can not be made to an entity controlled by relatives within the fourth degree of consanguinity or second degree of affinity, and individuals with an Act 22-2012 grant.

Caroline López, CPA, Esq.

Tax Manager

Collaborated in the preparation of this article.

We are committed to keeping you up to date with all tax-related developments. Please contact our Tax Department should additional information be required regarding this or any other tax issue. We will be glad to assist you.