The Puerto Rico Treasury Department released Internal Revenue Circular Letter 18-10 to establish the dates for the back to school tax free periods for the fiscal year 2018-2019 and also to establish the articles that will be exempt from Sales and Use Tax (“SUT”) during these periods.

The Back to School Tax Free Periods consist of two days in the month of July and two days in the month of January, during which uniforms and school materials will be exempted from payment of the sales tax at the state and municipal level.

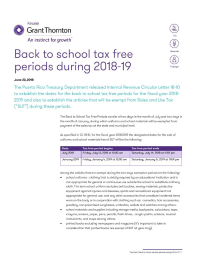

As specified in CL 18-10, for the fiscal year 2018-2019 the designated dates for the sale of uniforms and school materials free of SUT will be the following:

Date

|

Tax free period begins

|

Tax free period ends

|

|

July 2018

|

Friday, July 13, 2018 at 12:00 am

|

Saturday, July 14, 2018 at 11:59 pm

|

|

January 2019

|

Friday, January 4, 2019 at 12:00 am

|

Saturday, January 5, 2019 at 11:59 pm

|

Among the articles that are exempt during the two days exemption period are the following:

- school uniforms - clothing that is strictly required by an educational institution and is not appropriate for general or continuous use outside the school to substitute ordinary cloth. The term school uniform excludes belt buckles, sewing materials, protective equipment against injuries and diseases, sports and recreational equipment not appropriate for general use, and any other accessories that constitute incidental items worn on the body or in conjunction with clothing such as: cosmetics, hair accessories, jewellery, non-prescribed sunglasses, umbrellas, wallets and watches among others.

- school materials and supplies including storage media, backpacks, calculators, tape, crayons, erasers, paper, pens, pencils, flash drives, acrylic paints, scissors, musical instruments, and maps among others.

- printed books excluding newspapers and magazine (it’s important to take in consideration that printed books are exempt of SUT all year long).

- e-books as long as they are included in an official list from the educational entity (exempt all year long).

- notebooks

In order to be considered as an exempt transaction, any sale under a Lay Away program or purchase by internet, phone, or mail, must be fully paid, the title must be transferred to the buyer and the delivery is before the end of the exemption period.

Rain checks, gift cards and gift certificates used during the exemption period will qualify for the exemption. As a result, articles purchased with rain checks, gift cards or gift certificates during the exemption period will be exempt from SUT. Articles acquired before or after the exemption period will be subject to SUT, regardless of whether the gift card or gift certificate was purchased during the exemption period.

No special reporting is required for the exempt sales made during the exemption period Merchants should report all the qualifying sales on the Sales and Use Tax Return as exempt sales.

Please contact our Tax Department should you require additional information regarding this or any other tax issue. We will be glad to assist you.