Accountability in the financial reporting process

20 May 2019Audit is just one part of the assurance process. Around the world, auditors are responsible for a set of checks, but ultimately it is management who are responsible for the quality of information and what decisions are made as a result.

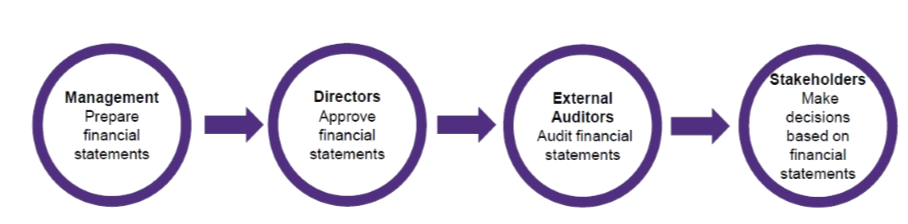

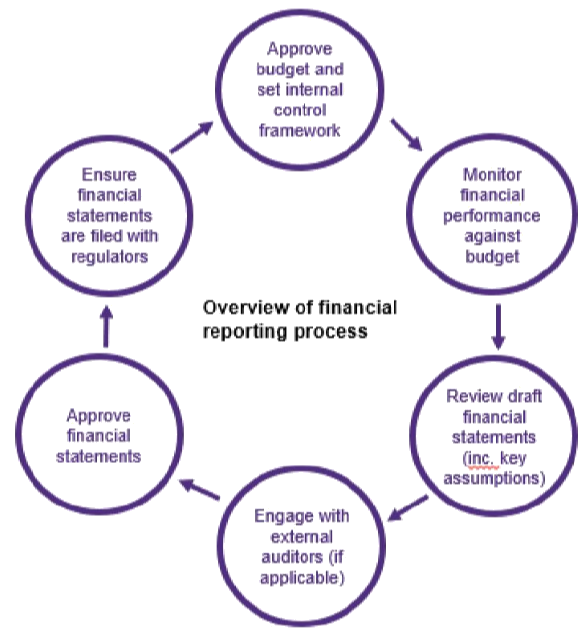

The overview below describes the system, according to the ACCA (Association of Chartered Certified Accountants a leading international accountancy body), demonstrating the role of management and directors in the financial reporting supply chain and the financial reporting process, which echoes in many jurisdictions around the world.

Key participants in the financial reporting supply chain

Regulators:

Review financial statements and oversee the performance of the directors and external auditors.

In addition, in some markets, there is a need for specific shifts in the regulatory regime. For example, the proposals in the Kingman Review in the UK to give audit regulators statutory powers – powers they already have in, for example, the USA – were broadly welcomed by the firms because the firms support robust, effective regulation.

As the financial reporting community explores how to change, it is important to focus on what will work in practice in a field that employs over a million people globally.

The effectiveness of audit depends on the ability to bring highly specialized skills to bear at scale. It depends on sustained investment in people and technology. The transformation needs to build on these platforms for success. Audit in particular, and assurance in general, is changing and needs to change further.

Source:

The public interest, accounting and the future of audit. A Guide to the Industry. GT Connect March 2019. ACCA Global: 2017 Guide to Directors: Responsibilities for Financial Reporting

We are committed to keep you updated of all developments that may affect the way you do business in Puerto Rico. Please contact us for further assistance in relation to this or any other matter.