-

Financial statements audits

Financial statement audits

-

Compliance audits

Compliance audits

-

Compilations and reviews

Compilations and audit

-

Agreed-upon procedures

Agreed-upon procedures

-

Corporate and business tax

Our trusted teams can prepare corporate tax files and ruling requests, support you with deferrals, accounting procedures and legitimate tax benefits.

-

International tax

Our teams have in-depth knowledge of the relationship between domestic and international tax laws.

-

Tax compliance

Business Tax

-

Individual taxes

Individual taxes

-

Estate and succession planning

Estate and succession planning

-

Global mobility services

Through our global organisation of member firms, we support both companies and individuals, providing insightful solutions to minimise the tax burden for both parties.

-

Sales and use tax and indirect taxes

SUT/ VAT & indirect taxes

-

Tax incentives program

Tax incentives program

-

Transfer Pricing Study

The laws surrounding transfer pricing are becoming ever more complex, as tax affairs of multinational companies are facing scrutiny from media, regulators and the public

-

Business consulting

Our business consulting services can help you improve your operational performance and productivity, adding value throughout your growth life cycle.

-

Forensic and investigative services

At Grant Thornton, we have a wealth of knowledge in forensic services and can support you with issues such as dispute resolution, fraud and insurance claims.

-

Fraud and investigations

The commercial landscape is changing fast. An ever more regulated environment means organizations today must adopt stringent governance and compliance processes. As business has become global, organizations need to adapt to deal with multi-jurisdictional investigations, litigation, and dispute resolution, address the threat of cyber-attack and at the same time protect the organization’s value.

-

Dispute resolutions

Our independent experts are experienced in advising on civil and criminal matters involving contract breaches, partnership disputes, auditor negligence, shareholder disputes and company valuations, disputes for corporates, the public sector and individuals. We act in all forms of dispute resolution, including litigation, arbitration, and mediation.

-

Business risk services

We can help you identify, understand and manage potential risks to safeguard your business and comply with regulatory requirements.

-

Internal audit

We work with our clients to assess their corporate level risk, identify areas of greatest risk and develop appropriate work plans and audit programs to mitigate these risks.

-

Service organization reports

As a service organization, you know how important it is to produce a report for your customers and their auditors that instills confidence and enhances their trust in your services. Grant Thornton Advisory professionals can help you determine which report(s) will satisfy your customers’ needs and provide relevant information to your customers and customers’ auditors that will be a business benefit to you.

-

Transaction advisory services

Transactions are significant events in the life of a business – a successful deal that can have a lasting impact on the future shape of the organizations involved. Because the stakes are high for both buyers and sellers, experience, determination and pragmatism are required to bring deals safely through to conclusion.

-

Mergers and acquisitions

Globalization and company growth ambitions are driving an increase in M&A activity worldwide as businesses look to establish a footprint in countries beyond their own. Even within their own regions, many businesses feel the pressure to acquire in order to establish a strategic presence in new markets, such as those being created by rapid technological innovation.

-

Valuations

We can support you throughout the transaction process – helping achieve the best possible outcome at the point of the transaction and in the longer term.

-

Recovery and reorganization

We provide a wide range of services to recovery and reorganisation professionals, companies and their stakeholders.

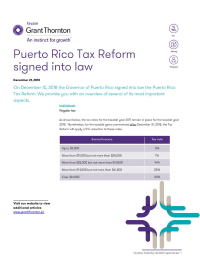

Puerto Rico Tax Reform signed into law

21 Dec 2018On December 10, 2018 the Governor of Puerto Rico signed into law the Puerto Rico Tax Reform. We provide you with an overview of several of its most important aspects.

Individuals

Regular tax

As shown below, the tax rates for the taxable year 2017 remain in place for the taxable year 2018. Nonetheless, for the taxable years commenced after December 31, 2018, the Tax Reform will apply a 5% reduction to these rates.

|

Earned Income |

Tax rate |

|

Up to $9,000 |

0% |

|

More than $9,000 but not more than $25,000 |

7% |

|

More than $25,000 but not more than $41,500 |

14% |

|

More than $41,500 but not more than $61,500 |

25% |

|

Over $61,500 |

33% |

Alternate Basic Tax (ABT)

For taxable years commenced after December 31, 2018, the tax rates will be the following:

|

Earned income |

Tax rate |

|

Over $25,000 but not more than $50,000 |

1% |

|

More than $50,000 but not more than $75,000 |

3% |

|

More than $75,000 but not more than $150,000 |

5% |

|

More than $150,000 but not more than $250,000 |

10% |

|

Over $250,000 |

24% |

The Reform allows a series of new deductions when computing the Alternate Basic Tax. Moreover, the Secretary of the Treasury will allow an individual to claim the totality of his/her ordinary and necessary expenses related to trade or business if its income tax return is filed with either an Agreed-Upon Procedures Report or Compliance Attestation report prepared by a Puerto Rico CPA.

Lastly, the ABT Credit is reestablished.

Optional Tax

The Reform introduces an Optional Tax structure for self-employed individuals who derive all of their income substantially from services that are subject to withholding at source. This optional tax will be computed on gross revenues without the benefit of operating expenses or personal deductions.

|

Earned income |

Tax rate |

|

Up to $100,000 |

6% |

|

More than $100,000 but not more than $200,000 |

10% |

|

More than $200,000 but not more than $300,000 |

13% |

|

More than $300,000 but not more than $400,000 |

15% |

|

More than $400,000 but not more than $500,000 |

17% |

|

More than $500,000 |

20% |

This optional tax will be available for taxable years commenced after December 31, 2018, although the Secretary of the Treasury may postpone its validity for taxable years commenced after December 31, 2019

Corporations

Regular tax

For taxable years commenced after December 31, 2018, the regular tax rate is reduced from 20% to 18.5%. Moreover, in the the case of taxpayers whose business volume is $3MM or more, the tax rate will be 23%.

Alternative minimum tax

The AMT will be the greater of $500 or 18.5% of the alternative minimum net income. Although the Reform imposes new limitations on deductible expenses to determine the net income subject to alternative minimum tax, it also provides for a taxpayer to claim all ordinary and necessary expenses if it submits audited financial statements, agreed upon procedures (AUP) or Compliance Attestation Reports by a CPA licensed to practice in PR.

|

Deductible expenses |

Requirement |

|

Salaries (125% deduction) |

W-2 |

|

Payments for services directly related to the trade or business |

Informative Return |

|

Contributions to health/accident plans for employees |

- |

|

Rents, Telecommunications, Internet |

Informative Return |

|

Utilities |

No limitation |

|

Advertising, Promotion and Marketing |

Informative Return |

|

Property, Contingency and Public Liability insurance |

Informative Return |

|

Depreciation under Straight-Line method |

No limitation |

|

Interest, Other Taxes, bad debts, contributions to employee trusts or deferred payment plan, charitable contributions, agricultural income |

- |

Optional tax

Same as with Individuals, the Tax Reform allows an Optional Tax computation for Corporations, if the following three (3) requirements are met:

- total gross income is substantially derived from services rendered,

- total gross income was reported on informative returns, and

- total gross income was subject to withholding at source or estimated tax payment

If the optional computation is elected, taxpayer will not be able to claim expenses or deductions and will not be subject to the required reports.

The applicable rates will be as follows:

|

Earned income |

Tax Rate |

|

Up to $100,000 |

6% |

|

More than $100,000 but not more than $200,000 |

10% |

|

More than $200,000 but not more than $300,000 |

13% |

|

More than $300,000 but not more than $400,000 |

15% |

|

More than $400,000 but not more than $500,000 |

17% |

|

More than $500,000 |

20% |

Deductions

- depreciation

- business with volume of $3MM or less, may compute the deduction using a useful life of two (2) years for fixed assets used in the trade or business

- exception: real property and automobiles

- business with volume of $3MM or less, may compute the deduction using a useful life of two (2) years for fixed assets used in the trade or business

- automobiles

- for payments made after December 31, 2017, allows the deduction for actual expenses incurred for use and maintenance subject to a limit that will be established through Regulations

- deduction for mileage established by the Secretary will never be less than the one established by the IRS

- charitable contributions

- for taxable years beginning after December 31, 2018, a deduction will be allowed for charitable contributions made to non for profit entities certified by the Secretary of Treasury or by the IRS that provide services to residents of PR

- Net Operating Losses (NOL)

- the 90% limitation is reestablished for tax years beginning after December 31, 2018

- the NOL will include expenses for payments made to related entities not engaged in business in PR and not subject to withholding

- pass-through entities losses

- reestablishes the limitation to 90% of the share of net income in similar entities for tax years beginning after December 31, 2018

- employment of young college students/recent graduates.

- establishes a 150% deduction on salaries paid to college students and recently graduated individuals who are employed for at least 20 hours a week for a period of 9 months or 800 hours a year, at a rate over $10/hour

- 200% deduction in the case of students who come from the internship program at the Department of Treasury

- non-deductible items

- for tax years beginning after December 31, 2018, the 51% disallowance on charges between related entities is eliminated if the taxpayer files a transfer pricing study along with its income tax return.

- the transfer pricing study must be prepared in accordance with §482 of the U.S. Internal Revenue Code, as amended.

- for tax years beginning after December 31, 2018, the 51% disallowance on charges between related entities is eliminated if the taxpayer files a transfer pricing study along with its income tax return.

Tax returns

- only one signature will be required from the President, Vice-President, Treasurer, Assistant Treasurer or other principal officer

- if the total tax on gross income was paid through withholding at source, the corporation will not be required to file a tax return

- for taxable years beginning after December 31, 2016, the automatic extension granted will be for a period of six (6) months, instead of three (3) months

Tax payments

- the Secretary may prescribe that tax payments be made solely through electronic means.

Estimated tax

- the amount due will be the lesser of 90% of such year’s tax, or:

- tax determined on the prior year tax return, or

- tax calculated at the tax rates and under the rules applicable to such year using the data included in the prior year tax return.

Sales and Use Tax (SUT)

- effective October 1, 2019, the SUT on prepared food sold by restaurants will be reduced to 7%

- restaurants = all commercial establishments, including food trucks, that sell food and drinks, as long as it is served hot and/or with eating utensils

- alcoholic drinks are not included

- some definitions are modified to include additional services that need to paid SUT over the price charge

- Admission Rights – include fees and charges paid to private or membership clubs that provide facilities for the purchase of goods or services

- Legal Services – those provided by members of the legal profession authorized by the Puerto Rico Supreme Court to practice, or by a corresponding entity in a foreign jurisdiction, only with respect to fees for services related to legal representation before the Courts or administrative agencies, consulting and notarial services

- Sales Price – in the event that a product is sold with discounts or rebates from the manufacturer or wholesaler, who then reimburses the difference, the manufacturer or wholesaler will be obliged to reimburse, along with the discount, an amount equal to the sales tax that would result if said refund were a sale

- some SUT exemptions were modified

- lease of real property – evidence of compliance with requirements to maintain a fiscal terminal, if necessary, is required

- lease and purchase of machinery, material, equipment, etc., used in providing health services

- electronic books – applies to both purchase and rent

- B2B and designated professions services provided by person whose annual business volume does not exceed $200,000

- effective March 1, 2019

- personal hygiene products for women

Please contact our Tax Department should you require additional information regarding this or any other tax issue. We will be glad to assist you.