-

Financial statements audits

Financial statement audits

-

Compliance audits

Compliance audits

-

Compilations and reviews

Compilations and audit

-

Agreed-upon procedures

Agreed-upon procedures

-

Corporate and business tax

Our trusted teams can prepare corporate tax files and ruling requests, support you with deferrals, accounting procedures and legitimate tax benefits.

-

International tax

Our teams have in-depth knowledge of the relationship between domestic and international tax laws.

-

Tax compliance

Business Tax

-

Individual taxes

Individual taxes

-

Estate and succession planning

Estate and succession planning

-

Global mobility services

Through our global organisation of member firms, we support both companies and individuals, providing insightful solutions to minimise the tax burden for both parties.

-

Sales and use tax and indirect taxes

SUT/ VAT & indirect taxes

-

Tax incentives program

Tax incentives program

-

Transfer Pricing Study

The laws surrounding transfer pricing are becoming ever more complex, as tax affairs of multinational companies are facing scrutiny from media, regulators and the public

-

Business consulting

Our business consulting services can help you improve your operational performance and productivity, adding value throughout your growth life cycle.

-

Forensic and investigative services

At Grant Thornton, we have a wealth of knowledge in forensic services and can support you with issues such as dispute resolution, fraud and insurance claims.

-

Fraud and investigations

The commercial landscape is changing fast. An ever more regulated environment means organizations today must adopt stringent governance and compliance processes. As business has become global, organizations need to adapt to deal with multi-jurisdictional investigations, litigation, and dispute resolution, address the threat of cyber-attack and at the same time protect the organization’s value.

-

Dispute resolutions

Our independent experts are experienced in advising on civil and criminal matters involving contract breaches, partnership disputes, auditor negligence, shareholder disputes and company valuations, disputes for corporates, the public sector and individuals. We act in all forms of dispute resolution, including litigation, arbitration, and mediation.

-

Business risk services

We can help you identify, understand and manage potential risks to safeguard your business and comply with regulatory requirements.

-

Internal audit

We work with our clients to assess their corporate level risk, identify areas of greatest risk and develop appropriate work plans and audit programs to mitigate these risks.

-

Service organization reports

As a service organization, you know how important it is to produce a report for your customers and their auditors that instills confidence and enhances their trust in your services. Grant Thornton Advisory professionals can help you determine which report(s) will satisfy your customers’ needs and provide relevant information to your customers and customers’ auditors that will be a business benefit to you.

-

Transaction advisory services

Transactions are significant events in the life of a business – a successful deal that can have a lasting impact on the future shape of the organizations involved. Because the stakes are high for both buyers and sellers, experience, determination and pragmatism are required to bring deals safely through to conclusion.

-

Mergers and acquisitions

Globalization and company growth ambitions are driving an increase in M&A activity worldwide as businesses look to establish a footprint in countries beyond their own. Even within their own regions, many businesses feel the pressure to acquire in order to establish a strategic presence in new markets, such as those being created by rapid technological innovation.

-

Valuations

We can support you throughout the transaction process – helping achieve the best possible outcome at the point of the transaction and in the longer term.

-

Recovery and reorganization

We provide a wide range of services to recovery and reorganisation professionals, companies and their stakeholders.

Loan restructurings with periods of reduced payments

16 Sep 2020In response to COVID-19, many creditors are engaging in a variety of programs to restructure their borrower’s loans in various ways, including payment deferrals, fee waivers, and extension of repayment terms, which may result in periods of reduced payments following the restructuring, such as payment holidays. On June 30, 2020, the AICPA issued Technical Question and Answer (TQA) 2130.41 addressing the subsequent accounting for these types of restructurings, provided the restructuring is neither a troubled debt restructuring (TDR) nor accounted for as a new loan.

Determining the EIR for non-TDRs

As noted in the TQA, if a restructured loan is not required to be accounted for as a TDR or as a new loan, then it is accounted for as a restructuring and continuation of the original loan under ASC 310-20, Receivables – Nonrefundable Fees and Other Costs. For such loan, a new effective interest rate (EIR) is determined and applied prospectively in accordance with the interest method prescribed by the guidance in ASC 310-20. The objective of the interest method is to arrive at periodic interest income at a constant EIR on the net investment in the loan over the loan’s contractual life. In general, the new EIR is the rate that equates new contractual cash flows over the restructured contractual term with the amortized cost basis of the loan at the restructuring date.

FASB technical inquiry

For restructured loans with periods of reduced payments following a restructuring, applying the interest method may cause the amortized cost basis of the restructured loan to exceed the amount for which the borrower could settle the loan during the periods of reduced payments, as illustrated in Example 6 in ASC 310-20-55-35 through 55-37 (see below). Loans originated with increasing rates are subject to the guidance in ASC 310-20-35-18(a), which prohibits recognizing interest income that would result in a creditor’s net investment in a loan increasing above the amount for which the borrower could settle the obligation.

During the April 8, 2020, FASB meeting, the FASB staff discussed a fact pattern in which a loan was restructured in response to COVID-19 and (1) the restructuring was neither a TDR nor accounted for as a new loan, and (2) the restructured terms included a period with reduced payments. The FASB staff indicated that a creditor may either elect to apply, or not to apply, the guidance in ASC 310-20-35-18(a) to these loans. The TQA indicates that the election must be made as an entity-wide accounting policy.

Electing to apply ASC 310-20-35-18(a)

If a creditor elects to apply the guidance in ASC 310-20-35-18(a) to its restructurings that include periods of reduced payments and are neither TDRs nor accounted for as new loans, the EIR on the restructured loan would be the rate that equates the new contractual cash flows over the restructured contractual term with the amortized cost basis of the loan at the restructuring date. However, the amount recognized in interest income is limited to the amount that would not cause the creditor’s amortized cost basis in the loan to exceed the amount for which the borrower could settle the obligation. The determination of, and accounting for, this limitation is illustrated in Example 6 in ASC 310-20-55-35 through 55-37 (see below).

At the end of the period of reduced payments, the creditor determines a new EIR, in accordance with the guidance in ASC 310-20, that equates the remaining contractual cash flows to the amortized cost basis of the loan.

Other considerations

TQA 2130.41 also notes that whichever accounting policy the creditor elects, if it has elected to estimate prepayments in accordance with ASC 310-20-35-26 through 35-32, it should consider the impact of that guidance on its determination of the EIR.

Additionally, whichever accounting policy the creditor elects, the creditor should apply appropriate accounting policies for recognizing interest income to restructured loans when concerns about the realization of loan principal or interest exist.

Example 6 shown below has been excerpted from the FASB Codification.

ASC 310-20-55-35 through 55-37

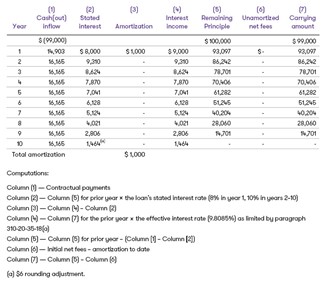

Example 6: Application of Paragraph 310-20-35-18(a)—With No Prepayment Penalty

This Example illustrates the guidance in paragraph 310-20-35-18(a) for the application of the interest method of amortization with an increasing rate loan and with no penalty charged for prepayment of principal. This Example has the following assumptions.

Entity F grants a 10-year $100,000 loan. The contract provides for 8 percent interest in Year 1 and 10 percent interest in Years 2-10. Entity F receives net fees of $1,000 related to this loan. The contract specifies that no penalty will be charged for prepayment of principal.

The discount factor that equates the present value of the cash inflows in Column 1 with the initial cash outflow of $99,000 is 9.8085 percent. In Year 1, recognition of interest income on the investment of $99,000 at a rate of 9.8085 percent would cause the investment to be $93,807, or $710 greater than the amount at which the borrower could settle the obligation. Because the condition set forth in paragraph 310-20-35-18(a) is not met, recognition of an amount greater than the net fee is not permitted. The loan would be accounted for as follows.

Source:

Grant Thornton, On the Horizon July 9 2020

We are committed to keeping you up to date of all developments that may affect the way you do business in Puerto Rico. Please contact us for further assistance in relation to this or any other matter.